IIMM Series : KYC - Know Your Cycle(s) !

Howard Marks said '...just about everything is cyclical'. Understanding the concept of 'cycles' is very important for an investor to position themselves for better returns.

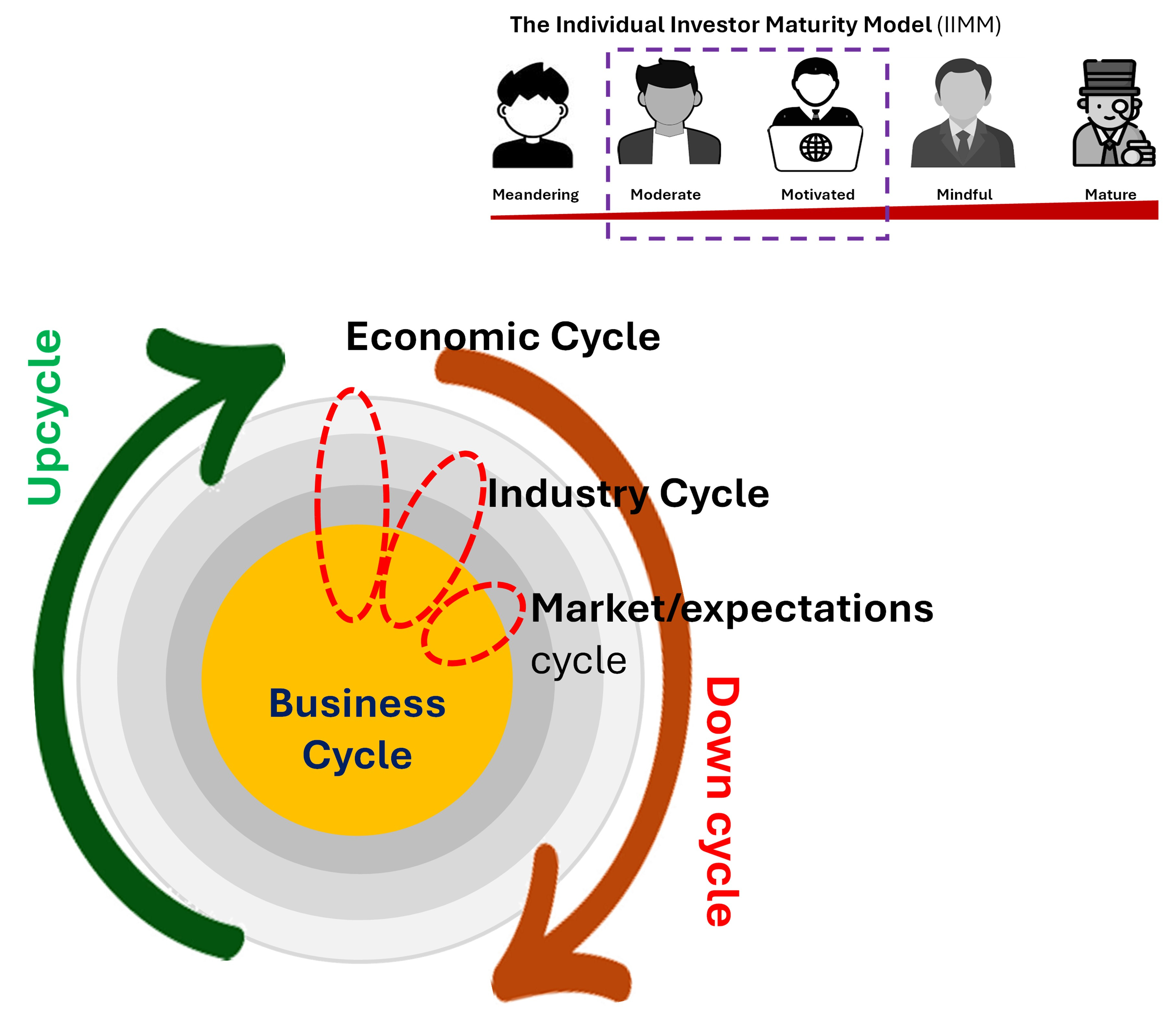

(This point of view is addressed towards ‘moderate’ and ‘motivated’ investors from the IIMM - Individual Investor Maturity Model)

https://venupsv.substack.com/p/the-individual-investor-maturity/comments

Businesses exist and perform in an environment. When evaluating businesses for investing, fundamental analysis equips investors with an understanding of the ‘top-down’ environment/context i.e. economy, industry, segment. While these dimensions are known to have their ups and downs i.e. ‘cyclicality’ is in their construct, investors often forget and/or behave as if these are ‘linear’, thereby ignoring or extrapolating current environment, respectively. This leads to sub-optimal results from stock picking, due to investor actions derived from either FOMO or JOMO.

Stock prices ‘ebb and flow’ against the backdrop of multiple influencing cycles of the environment. Understanding the layers and their cycles will help an investor position themselves to improve their chances of getting better returns. Here is a deep dive on ‘cycles’ that impact stock prices.

a. Economic Cycle : This cycle is the natural cycle with defined phases of ‘expansion-peak-contraction-recovery’, that repeats. It impacts : GDP, per capita income, wealth pyramid and trickles down to business specific parameters such as addressable market (via disposal income). Possibly this is the ‘longest’ cycle and can run across multiple years while having a significant impact also on type of businesses (that outperform) and their valuations. As an example, the economic cycles of USA and Japan over the last 40-60 years contrast, clearly impacting the performance of their financial markets (indices and constituents). In addition, anchors of economy i.e. the Government and the Central Bank, often working in tandem, support economic cycles with fiscal (incl. taxation) and monetary policies (interest rate, liquidity) respectively. Derived from monetary policy, interest rate cycle (rising and falling) impacts cost of funds for businesses and market participants (risk free + risk premium) and discounting rate for returns. These policy actions can create, extend cycles. More often they tend to bolster stock / asset prices, than not. They also create boom - bust cycle in asset prices, across the board. Sovereign ratings, often a reflection of a country’s economic cycle, also nudge the cycle. Thus, an investor needs to position to benefit from the economic cycle of target markets. For example - in a lower interest rate cycle investor may load up on those that benefit from benign cycle e.g. lenders, real estate firms, consumption plays. Conversely, investors can also hedge against an upcycle of inflation & interest rates by shifting to sectors such as FMCG, leaders (with pricing power). Structurally, investors can also position into economic cycle of the country based on drivers - industrialization (manufacturers), financialization (AMCs, wealth management, FMIs), service transformation (IT/ITEs) etc, typically termed as ‘mega-trends’.

b. Industry Cycle: Broadly two cycles exist - inter and intra industry cycle. ‘Inter’ industry cycles constantly evolve giving select industry (sectors) greater valuations versus others e.g. sunrise sectors gain better multiples and drift down. Overtime, mature industries settle down to lower band of valuation. e.g. railroads, FMCG, power utilities. This is primarily due to capability, capacity built by industry participants, alongside industry specific return profile (costs, growth, margins, capex etc.). ‘Intra’ industry cycles are driven by sector dynamics such as pricing power, input cost cycle (e.g. commodity cycles), capital investment, structure (one v. many vs few e.g. oligopoly) and more. The primary one though is ‘capital cycle’1 as elucidated by Edward Chancellor. The continuous entry and exit of competitors into businesses with returns, thereby impacting ‘moat’, is a natural cycle of capitalism. Indian market, for example, has seen new capital entering paints, wires sectors, thereby impacting stock prices of incumbents, downwards. Inversely, exit of players in airlines sector, pushed the market leader’s stock to newer highs ! Another structural ‘intra-industry’ cycle is also the transition of market share from un-organized to organized that typically gives a long runway to organized and well run players in sectors such as e.g. jewelry, paints, electricals, restaurants, edible oils.

c. Market (expectations) Cycle : This cycle reflects the expectations of market participants, both in anticipation and as a reaction to other cycles. Accordingly, valuations (P/E) expand and contract. At times, they are front loaded (optimistically) or rear ended (waiting for actual performance/numbers to show up 2. Events such as election of a business-friendly government, upgrade/downgrade by fund houses could trigger / accelerate expectations leading to higher valuations both at a sector level or its constituents, or both. Investors must gauge this at all times. Late entry into the expectation cycle, means, holding the bag and waiting for long time to get the entry price or target gains. As a corollary, early entry also means living with near to medium term underperformance , where gains may arrive at the rear end. Market participants also drive another cycle- ‘sector rotation’. Money moves to sectors that are most promising from those that are out-of-favor/likely to struggle, in the near term. This then raises / suppresses valuations.

d. Business Cycle: This is the closest cycle to impact a stock price. The net effect of all the above ‘upper’ cycles percolate/trickle down to this cycle. As we know, in the long run, stock prices reflect value generated by the business (weighing machine as called out by Mr.Buffett). Investors must focus on this cycle the most. A business’ own cycle(s) includes various factors such as investment (CAPEX, Working capital), debt (e.g. Indian Infrastructure firms went kaput under heavy debt in 2008-2015 cycle), people (incl. CEO/key people), input cost (e.g. oil price for paints industry, khopra price for coconut oil ) commodity cycle, cash conversion cycle, product pipeline/mix (incl. approvals for regulated products e.g. ANDA for pharma industry), ownership (reputed owners taking over e.g. in industrial power by a reputed group, batteries by FMCG leader), asset positioning (heavy/light), cost position (low cost to income ratio in banks), execution, innovation etc. All these impact earnings, which then impact stock prices. Based on the degree of impact of ‘economic cycle’, businesses do get branded as ‘cyclical’ with earnings and stock pricing rising and falling with some lead/lag e.g. metals, capital goods, ship builders. Incrementally, a business’ cycle also impacts the need for capital and is also cyclical resulting in capital raise or return of capital by way of dividends, buy-back etc.

We can go on and on…..

What’s Common?

a. The cycles are interlinked and they are turning continuously. This continous interplay leads to ‘alignments’ between two or all cycles, at a given time period. Aligned cycles lead to ‘consensus narrative’ about a business and consequently its valuation, that is valid for that alignment/duration, which by extension, is also subject to change.

b. The duration of each type of cycle is different. The cycles closer to business cycle are shorter and farther ones are longer/structural.

c. Stock prices can move based on shifts in one or more cycles. Total alignment across cycles, can lead to potential of extended value.

d. Across one’s portfolio, impact of a cycle can also be opposite. e.g. a price rise in a commodity impacts its producer business and user business differently.

How can investors navigate and benefit (takeaways) from KYC ?

a. Anticipate alignment and position for it. Act on events, especially those from capital cycle. Remember that what goes down also goes up and vice versa.

b. Upcycles are with tailwinds. Investors must remind themselves of the ‘rising pond-effect’ (as explained by Mr. Munger) and pare new investments or stagger them as per valuations. Similarly, investors need a plan for handling ‘down market’ cycles.

c. Gauge the impact / loading of the effect (front loaded /rear ended) to enable entry/exit along with extent of effect (relative movement e.g. similar to beta).

d. Asset allocation is a hedge for returns since economic cycle management leads to/supports inter-asset co-relation/divergence.

e. Develop active patience. If the price quoted by Mr.Market, on a daily basis, is not as per investor’s expectation, decline/walk away. Wait for trends to play out, if entry is delayed/missed. FOMO kills. Be mindful of ‘reversion to mean’, both ways.

f. Cycle timelines may not match expectations. Markets tend to overshoot, both ways.

g. Gauge for business performance in both favorable and non-favorable ‘upper’ cycles. These tend to indicate (in)elastic demand, pricing power i.e. pass through costs, cost management (fixed to variable costs) and other levers that drive moats. If some businesses defy the cyclicality, better than relative businesses, they may have cracked the code on anti-fragility3. Remember that, over time, business performance metrics drive stock prices.

h. Misalignment between cycles, leads to ‘anomalies’4. Investors can then take advantage of overpricing / underpricing based on the anomaly direction . (This is not easy and takes skill to identify and act. Timing could be broadly ok, and not precisely).

In summary, over time, an investor must evolve to knowing-the-cycle(s) to benefit from them.

Capital Returns: Investing Through the Capital Cycle: A Money Manager’s Reports 2002-15 by Edward Chancellor

https://collabfund.com/blog/expectations-debt/ by Morgan Housel

https://www.goodreads.com/book/show/13530973-antifragile

Mohnish Pabrai ‘anomalies’ - https://www.valueinvestordaily.com/p/value-investor-daily-14

Great article! Can relate to so many of these points (examples of specific stocks come to mind in certain periods)